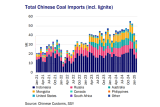

The IEA’s latest coal forecast presents a cautious outlook despite stronger-than-expected global coal trade in 2024. While their year-ago thermal coal trade forecast predicted a 12% decline for 2024, current estimates for global trade last year are 2-3% growth. Despite severely underestimating 2024 thermal coal trade, the IEA once again predicts a significant 8% decline in 2025. It is a similar story for coking coal, where, despite also surprising to the upside in 2024, IEA’s forecast has been downgraded to an expected 7% slowdown in 2025.

Despite these predictions of major changes, the underlying reasoning appears uncertain at best. Stronger -than-expected import demand for the past year, coupled with the resilience of key exporters at current prices, suggests that coal may remain central to the energy mix for at least another year. While current CFR South China (4,700 kcal) prices of $80/t are sharply down from the energy-crisis levels of 2021/22, they remain healthy compared to the 2011—2020 average of around $63/t.

The IEA expects Chinese electricity demand to grow a strong 6% per year through 2027 and also that coal-fired power generation will continue rising. However, they are also of the opinion that renewable energy will be able to fulfil most of this additional demand and that growing domestic coal supply will reduce the need for imports.

However, the uncertainty created by the increasing share of renewable energy generation is considerable. IEA’s forecast for Chinese coal consumption in 2027 is subject to an approximate +/- 140 Mt range under weak and strong performance scenarios for combined hydro, wind, and solar power generation. Given that coal consumption increased by an estimated 73Mt in 2024 for comparison, such massive uncertainty naturally creates an extremely wide distribution of outcomes also for Chinese coal trade, including the possibility that coal imports will continue to play a key role in balancing the country’s energy needs for longer.

With regards to the 2025 outlook, recent news of policy changes for the Chinese power generation industry seems to have been neglected. In 2024, Chinese authorities required generators to secure all of their annual domestic coal demand from the domestic term market. However, with improved stockpiles and supply of coal on international markets, officials have now reduced the requirement to 80% for 2025, signalling less concern about supply security and price volatility.

Going forward, this policy change should support increased spot market activity, with an increasing potential for growth in imports. McCloskey reported last month that China’s thermal coal term deals were heavily lagging 2024 levels. Many generators were reportedly hesitating to sign long-term deals with domestic miners as current term contracts remain too costly compared to imports. However, entering into international term contracts comes with its own set of challenges amid concerns that strained ties with the incoming US Trump administration may cause the Chinese RMB to weaken further.

Finally, the increasing number of coal-fired power projects being built on the coast will likely continue supporting a high pace of imports for the next few years. Around 30-40% of coal plants (in MW) built in the past two years have been in coastal provinces. Most of these power plants tend to blend different qualities of coal and are unlikely to solely depend on domestic supplies.

By Hamid Agassi, Dry Bulk Analyst, Research, SSY.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business