On 4th February, the Customs Tariff Commission of the State Council in China announced several new tariffs on imports from the US in retaliation to the US imposition of a flat 10% tariff on Chinese imports. Included in the new Chinese tariffs was an additional 15% tariff on coal imports to be applied after existing tariffs, meaning a total tariff of 18% on US coking coal (up from 3%) and 22% on US thermal coal (up from 6%).

China imported 12.1 Mt of coal from the US in 2024, equivalent to 2.2% of their total, including overland trade from Mongolia (which made up 15.3%). However, thanks to the long-haul nature of the trade, in tonne-mile terms the US-China coal trade made up 11.2% of Chinese coal vessel demand and 2.6% of global coal vessel demand.

The tariff impact will depend on the extent to which US coal is priced out of the Chinese market, where the US coal is shipped to if it does not go to China, and where China sources any replacement volumes from. Coking coal is the main focus here, with 10.7 Mt of the US coal imported by China in 2024 of that grade (87.9% of total).

The chart below compares the landed price of US coking coal in China (including freight and existing tariff) to Australian coking coal (a key benchmark that attracts no tariff thanks to a China-Australia trade deal from 2014). We note that Chinese imports of US coking coal picked up when pricing made it the more attractive option. Moreover, had the new tariff levels been in place, all else being equal, this arbitrage window would never have opened. On this basis, it seems likely that US coking coal will now be priced out of the Chinese market going forward. A similar argument can be made for US thermal coal, when comparing it to Indonesian thermal coal.

Whilst the increased price will reduce US-China trade generally, it’s also worth noting that there is a precedent for political pressure to reduce imports further. For example, when China put in place retaliatory tariffs on US soybeans in 2018, this trade fell to just 842 Kt in 2H18, down a massive 94% y-o-y.

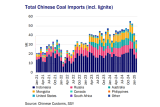

The worst case scenario for the dry bulk market would be if China replaced the lost US coking coal volumes with domestic resources or overland trade from Mongolia or even Russia. Although Mongolian coal exports to China have grown quickly (see above chart) further increases would be constrained by production growth. Similarly, with few viable alternatives, a large proportion of Russian coking coal is already going to China.

A more likely outcome is that India takes the US coking coal volumes, freeing up Australian coking coal export capacity to supply China. India seems to be enjoying a good trading relationship with the new US president, and government officials are talking of cutting tariffs rather than adding to them. US coking coal exports to India have grown from a low of 3.2 Mt in 2021 to around 9.5 Mt in 2024. Meanwhile, Australian exports to India have fallen from 54.3 Mt in 2021 to 34.4 Mt in 2024.

Using 2024 numbers, in a scenario where all US-China coking coal trade went to India instead, displacing some Australia-India trade to China, we estimate that total tonne-mile demand for the dry bulk fleet would have been lower by 44 Bn tonne miles (TM), bringing overall coal tonne-mile demand down to around 6,730 BnTM and reducing total bulker demand growth from 4.8% y-oy to 4.6% y-o-y. Interestingly, whilst this is a net negative for the market, it may turn out to be positive for the Capesize fleet and disproportionately negative for the Panamax fleet. In 2024, 39% of US coal exports to India went in Capesize vessels, compared to just 23% to China. Assuming the same split by vessel size, and again using 2024 numbers, the scenario adds 19 BnTM to Capesize demand whilst removing 58 BnTM from Panamaxes. Again, all other things being equal, this would have pushed total Capesize demand growth to 3.9% y-o-y from 3.7% in 2024 and Panamax growth down to 8.0% from 8.8%.

By William Tooth, Senior Dry Bulk Analyst, Research, SSY.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business