Our view on the measures proposed by the USTR to counter unfair Chinese trade practices in the maritime, shipbuilding and transportation sector.

The shipping industry is abuzz with discussions, forecasts and predictions about the impact of the proposed new US trade policies. These policies seem to be changing way too frequently and erratically for the markets’ liking, but for the argument’s sake let’s assume this is just because they are being fined-tuned to work better.

One of the most unexpected and shocking measures has been the proposed port entry fees of up for Chinese-built or Chinese-flagged vessels, with the goal to address China’s unfair trade practices in the maritime, logistics and shipbuilding sectors. The proposal was published on 21 February and was open to public comments till 10 March, after which a decision about the specifics will be made by 24 March. It is quite vague and some of its provisions are contradictory, but a few key points have captured the shipping industry’s attention. Here is a short summary of these:

- For each US port call, Chinese operators will be charged:

- A fee of to $1 million for any vessel operated by the company; or

- A fee of up to $1,000 per net ton of the vessel’s capacity

- For each US port call operators of Chinese-built vessels will be charged:

- A fee of up to $1.5 million; or

- A sliding-scale fee based on the percentage of Chinese-built vessels in the operator’s fleet:

- Operators with 50% or more of Chinese-built vessels – up to $1 million

- Operators with 25% to 50% of Chinese-built vessels – up to $750 thousand

- Operators with less than 25% of Chinese-built vessels – up to $500 thousand

- Additional port call fees for operators, based on the percentage of newbuilding orders they have from Chinese shipyards:

- a fee of up to $1,000,000 per vessel entrance to a U.S. port will be charged to a vessel operator with 25% or more of the total number of vessels ordered by that operator, or expected to be delivered to that operator, are ordered or expected to be delivered by Chinese shipyards over the next 24 months.

- A sliding-scale fee based on the percentage of vessels ordered from Chinese shipyards:

- operators with 50% or more of their vessel orders in Chinese shipyards or vessels expected to be delivered by Chinese shipyards over the next 24 months – up to $1 million per port call

- operators with 25% to 50% of their vessel orders in Chinese shipyards or vessels expected to be delivered by Chinese shipyards over the next 24 months – up to $750 thousand per port call

- operators with 25% to 50% of their vessel orders in Chinese shipyards or vessels expected to be delivered by Chinese shipyards over the next 24 months – up to $500 thousand per port call

Aiming to support US shipbuilding and maritime transport, the proposal also outlines requirements for US exports in the future:

- Effective as of the date of action, the international maritime transport of at least 1% of U.S. products, per calendar year, that is exported by vessel, will be restricted to export on U.S.-flagged vessels by U.S. operators.

- Effective as of 2 years following the date of action, the international maritime transport of at least 3% of U.S. products, per calendar year, that is exported by vessel, is restricted to export on U.S.-flagged vessels by U.S. operators.

- Effective as of 3 years following the date of action, the international maritime transport of at least 5% of U.S. goods, per calendar year, that is exported by vessel, is restricted to export on U.S.-flagged vessels by U.S. operators, of which 3 percent must be U.S.-flagged, U.S.-built vessels, by U.S. operators.

- Effective as of 7 years following the date of action, the international maritime transport of at least 15% of U.S. goods, per calendar year, is restricted to export on U.S.-flagged vessels by U.S. operators, of which 5% must be U.S.-flagged, U.S.-built vessels, by U.S. operators.

- S. goods are to be exported on U.S.-flagged, U.S.-built vessels, but may be approved for export on a non-U.S.-built vessel provided the operator providing international maritime transport services demonstrates that at least 20% of U.S. products, per calendar year, that the operator will transport by vessel, will be transported on U.S.-flagged, U.S.-built ships.

The US plans to push its allies and partners to enact similar measures or risk retaliation. Experts are already predicting legal challenges if such a rule comes into effect. Apart from that, it has been reported that the public comments on this policy proposal have been overwhelmingly negative, so if the administration takes them into account, it should come up with significantly milder final version.

No doubt, the suggested policy sounds scary.

But how practical is it, really? Can it be enforced? And if it can – what will be the impact on the shipping market? Below are some thoughts.

Chinese operators and Chinese-flagged ships

Taxing companies based on their nationality or where their assets are registered is probably a lost cause because of the very flexible nature of the shipping business. As it has become increasingly evident over the past few years when sanctions were targeting the Russian fleet, ships seamlessly changed ownership, as new companies sprang into existence around the world, specifically dedicated to avoiding the sanctions regime.

Changing a ship’s flag is relatively inexpensive and generally costs from a few thousand to tens of thousands of dollars. And if it is going to save millions on port fees, then it’s definitely worth doing it. And indeed some Chinese owners have already started changing their vessel flags. To disincentivize the owners from skirting the rule it would make sense the port call fee to be sufficiently low.

Chasing and enforcing this proposed rule on a global basis will be unsuccessful or will have very limited success, despite any retaliation threats from the US.

Chinese-built existing vessels

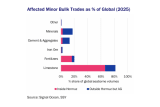

Unlike company’s domicile or ships flag, the country of built of an existing vessel cannot be changed, so this will be an easy target for the rule to be applied against. But is it such a big threat as it appears? Here is the math:

- Out of the entire IMO tanker fleet (5105 vessels) about 24% or 1,231 ships are built in China.

- Unless they are engaged in some long-term regional business in the US Gulf/Caribbean, the tankers that would usually call US ports have a capacity of at least 12,000t dwt. This narrows down the potential pool of targeted vessels to about 645.

- These 645 vessels made about 9,900 voyages in total in 2024 but only about 960 (or less than 10%) of these voyages had a US port as loading or discharging location.

- These 960 voyages were performed by about 233 ships. This represents about 4.5% of the whole IMO tanker fleet.

- Also, from the 233 vessels, 63% are above 45,000 dwt and 49% are epoxy-coated, so an easy replacement for those should be available.

- The 233 Chinese-built ships which called the US in 2024 were operated by 66 owners.

- However, out of these 66 owners, 31 had just 1 ship and another 8 had 2 ships engaged in trade with the US (a total of 47 ship) – these should be relatively easy to be replaced with other vessels from within the owners’ fleets or by taking on time charter.

- What is left then is a pool of 186 ships operated by 27 owners with 3 or more ships engaged in US trade.

- From these 186 ships, however, 85 are epoxy-coated – likely engaged in the CPP or vegoil trade – and in theory should be also easily replaceable.

- From the remaining 101 ships 40 are operated by 2 Norwegian and 1 Chinese owners.

- The Chinese owner who operates Chinese-built ships, will probably not be able to escape such port fees.

- But the Norwegian companies may get an exemption – even more likely because their ships are the classical parcel tankers and the so-called super-segregators. As such, they call multiple berths and ports within a single voyage. It is very typical for them to call 3-4 ports in the US Gulf to load or discharge cargo during the same voyage. If they were to be taxed at every port call, this would amount to additional costs of tens of dollars per metric ton of cargo transported – something which will surely drive an outcry from the business community.

- The remaining 61 vessels have marineline (49 ships), zinc (8 ships) and mixed coating (4 ships) and these are most likely trading methanol, CPP, biofuels and easy chemicals (aromatics, caustic soda, etc.). They will likely be the most affected by the proposed port fees.

- However, even these 61 ships (1.1% of the whole IMO fleet) may not be impacted because some of the owners operating them are US-based or with strong ties to the US. But with the possibility that the biofuels trade to and from the US may be severely downsized as the new administration rolls back biodiesel subsidies and imposes trade barriers to Chinese-origin products, and reciprocal tariffs on imports from other countries, the need for such ships calling US ports may be reduced anyway.

So, given the role of the US in the international chemical tanker trade, at most the impact on Chinese-built IMO-classed tanker vessels will be negligible.

The port call fees

For those who get caught in this rule, the suggested port fees are up to $1.5 million. However, the highest fees will likely apply to the biggest container ships. The IMO tankers, with their much smaller dimensions, have a good chance to get taxed at around the lowest range. The lowest proposed fee is $500 thousand, however if the final rule is watered down, this fee could easily be lower – possibly much lower.

If we assume $500 thousand would apply for an MR, then this is roughly $12/mt on a typical cargo size of 40,000 mt. As in other cases where the owners have to pay similar fees (EU-ETS, RefuelEU, etc.) those fees will be passed on to the charterers and ultimately to the end consumers. This may have implications for the spot trade where arbitrage opportunities to and from the US may be diminished. US chemical companies may strongly oppose such fees which they would deem as diminishing their competitive advantage. So, it is questionable whether and to what extent the proposed fees will be applied to chemical tankers.

Newbuildings at Chinese shipyards

Of the 66 operators whose vessels called US ports last year, only 6 with a total of 48 new ships by end 2027 will be affected by this rule. Out of these 6 operators, 4 are likely to get exemptions – the 2 Norwegian operators mentioned above and 2 oil majors. So, the direct impact or cost is also likely to be minimal.

Broder market implications

It is far from certain whether the proposed policy will be implemented, how and to what extent, but it does nevertheless raise red flags for the shipping sector which will lead to some shifts.

- Re-arranging of operator fleets to avoid sending Chinese-built or Chinese-flagged ships to the US.

- There may be some cancelations of newbuilding orders, however this will be very limited. The IMO fleet is big enough to be able to re-arrange according to point 1 above.

- Owners may be more cautious in their planning and place more orders at Korean, Japanese, or even Vietnamese and Turkish yards, which may lead to increased prices from those yards. At the same time, newbuilding prices from China may drop – and if combined with weaker yuan (as is already happening due to the tariffs from the US), this will make it even more attractive to order ships from China. So, overall orders at Chinese yards may not see such a steep decline as expected.

- US business and consumers will be paying more for imports. At the same time, US exports may become more expensive due to all these protectionist measures (tariffs, port fees, etc.)

- Reviving US shipbuilding is a long-shot goal which may be possible to achieve but only at immense cost, thus making the sector mostly uncompetitive. Asian shipbuilders have strong competitive advantages – lower labor and materials costs, highly skilled workforce, expertise and know-how from decades in the business, to name a few. The US may have a better chance at developing its shipbuilding with focus on high-value, specialized vessels such as cruise ships, oil rigs, LNG carriers, military vessels, etc. – similar to what other developed countries which have lost their shipbuilding industries to cheaper competitors have done (Germany or Singapore, for example).

While making good headlines, the suggested provisions for taxing Chinese-built or Chinese-flagged vessels may be less threatening for the chemical tanker market than expected. Quite possibly, the actual effect will be negligible, and the tanker market will be fully able to cope and re-arrange accordingly. However, the more real danger is that the highly erratic trade and economic polices coming from the new administration will cause overall reduced trade with the US – something which will not benefit anyone.

By Plamen Aleksandrov, Head of Research – Chemicals, SSY.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business