Global trade has reached the brink of another period of turbulence. Although the year 2025 has just begun, it has already made a significant impact, with Donald Trump’s presidency, and his immediate executive orders, the escalation of the US-China trade war, and a fragile ceasefire agreement between Israel and Gaza. It is clear that a new era is unfolding, and industries are facing fresh challenges, needing to navigate the changing landscape. It would not be wrong to say that everyone in the shipping industry is closely watching news of Donald Trump’s executive orders, trying to gauge how these might shift the global economy, and specifically the maritime sector. The new President has made it clear: trade between the USA and its trading partners will be reshaped by the potential implementation of tariffs on imports.

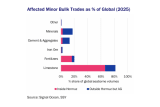

This time, the trade targets extend beyond China, with neighboring countries—Canada and Mexico—also facing the possibility of a 25% tariff starting February 1. These countries are highly dependent on the U.S. for their chemicals and plastics foreign trade. Although most of the liquid chemicals are transported by trains from Canada, and no direct impact is expected on waterborne shipping, the redirection of flows may present new opportunities for shippers. Trade in chemicals between the U.S. and Mexico is done by ships; however, Mexico has few economical alternatives if it were to limit its chemical imports from the U.S. in response to the tariffs. Therefore, Mexican demand for U.S.-origin chemicals may prove to be rather inelastic, and as such, may not see much change. It may even be the case that, due to lost market share in China, prices for some U.S. products may drop. In the end, Mexico may even increase its imports from the U.S. The outcome remains highly uncertain at this stage. The imposition of tariffs on goods coming from China is still under investigation, but the U.S. may apply a 10% tariff on these imports. In addition, inbound cargoes from the European Union have also been targeted, although the exact levy share remains unclear at this time.

While the re-elected U.S. President aims to protect domestic production through tariff impositions, he has also declared a National Energy Emergency to prioritize increased fossil fuel production and once again withdrew the country from a global climate agreement. The directive calls for agencies to expedite projects related to energy, energy infrastructure, and natural resources, including streamlining permitting processes. This also applies to pipelines and other transportation projects. Additionally, there will be a focus on improving transportation and refining infrastructure in the Northeast and West Coast. The U.S. chemical and plastics industries are expected to benefit from increased supplies of natural gas liquids (NGLs), which are essential for maintaining their global cost advantage in feedstocks. Furthermore, President Donald Trump instructed his administration to consider eliminating subsidies and policies that support electric vehicles, potentially slowing the adoption of cleaner cars in the U.S.

US-China tensions could intensify not only due to the implementation of tariffs but also from the blacklisting of the world’s largest shipbuilding group, China State Shipbuilding Corp (CSSC), and some of its affiliates. Additionally, the U.S. is investigating China’s efforts to dominate the maritime, logistics, and shipbuilding sectors. The U.S. has concluded that China’s pursuit of dominance in these sectors is unreasonable and burdens or restricts U.S. commerce. It is stated that today the U.S. ranks 19th in the world in commercial shipbuilding, constructing fewer than five ships annually, while China builds over 1,700 ships. In contrast, in 1975, the United States was ranked number one, producing more than 70 ships each year. With the U.S. President’s ambitious plans to reshape the country’s economy and its position in global trade, it is possible that the U.S. may begin investing in commercial shipbuilding to regain a leading role in the industry.

The beginning of 2025 has been eventful for both the chemical and shipping industries, with the USA making headlines but not being the only key player. In mid-January, Gaza and Israel reached a ceasefire agreement. Following this, Yemen’s Houthi rebels declared a truce in the Red Sea, announcing an end to their attacks on this crucial trade route. This decision is expected to reduce threats to shipping vessels in the area. However, the relief to the shipping industry may not be as tangible as it may seem. The Houthi leaders have strong incentives to continue their attacks and there will always be a threat that they may strike a vessel if they believe Israel is acting too aggressively or unfairly to the Arabs in its long-term policy to push the Arabs away and occupy their territories. Although few shipowners would likely want to expose their vessels to such risks, there could be an increase in the number of Chinese, Vietnamese, and possibly Japanese ships transiting the Red Sea.

The outcome may be beneficial for the shipowners who will start transiting the Red Sea again and can still reap relatively high freight rates, as there will still be limited supply of such ships, while making shorter voyages which means faster turnaround and more cargo transported. The Houthis may be able to collect more protection money from the increased number of vessels, while still holding the key to free navigation in the region. An increase in ship transits through the Red Sea promises higher revenue, which is badly needed for the Suez Canal. Producers with plants in the area will also benefit from more vessels available to load their cargoes. Owners who continue to route their ships via the Cape of Good Hope may keep enjoying sustaining high freight rates. Finally, insurance premiums may drop, though still not back to pre-conflict levels.

The beginning of 2025 has undeniably brought new challenges and new opportunities to the shipping industry. With such significant developments already unfolding, the next twelve months hold much uncertainty, but at the same time, potential benefits for global trade and maritime operations.

By Svitlana Synoha, Market Analyst – Chemicals, SSY.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business