The recent lack of Capesize scrapping has put renewed focus on the trading opportunities for the ageing part of the fleet. For instance, while the average age of scrapped Capesize (100k+ dwt) vessels over the past five years has been 23 years, Australian iron ore majors typically impose a maximum age of 15 or 18 years, while Brazil requires additional certification for vessels aged 18+ and North America similarly restricts on age. Until now, this has not caused any issues for older tonnage due to the strength of peripheral Cape demand. Russian and Ukrainian trades, in particular, have seen increased demand for older vessels due to their higher risk. However, with these trades potentially declining and more Capes due to fall into this older age bracket, as the vessels delivered during the post-2008 newbuilding boom turn 15, these vessels may be competing for less cargo.

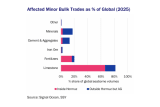

The average age of vessels employed in Russia and Ukraine trades has risen from 11 years old in 2021 to 18 in 2024, as the Russian invasion of Ukraine and Red Sea disruptions led to sanctioned and higher-risk trade, far exceeding the increase in the average age of the global fleet (from 9 years in 2021 to 11 years in 2024). However, while the use of 15+ year-old vessels used ex-Russia and Ukraine has increased, the Cape cargo volumes from the countries have recently declined. Overall coal exports from Russia have fallen 12% in the year-to-August compared to last year. This hides a further downward shift in tonne-miles, as shipments from Atlantic coast ports have fallen more than those from the Pacific. Partially as a result of shorter distances, the Cape share of Russian coal trade has fallen from 20% in 2022 to 15% in 2024. Meanwhile, Ukrainian iron ore volumes have not recovered back to their pre-war level and may decline further. The recent drop in the iron ore price comes amid Ukraine facing increasing energy costs as Russia destroys its infrastructure, and the country relies on purchasing EU energy at an elevated price. These cost pressures add to existing higher freight rates as Ukraine-China voyages require both a Ukraine and Suez Canal war risk premium.

Ultimately, the decision on the age of vessels used depends on the charterer. For the time being, the growing West Africa trades do not restrict by age, although older vessels are fixed at a discount, with the strongly growing Guinean bauxite trade absorbing substantial numbers of older vessels (15+ year-old vessels account for 40% ex-Guinea Cape trade by DWT). However, with the incoming jump in “overage” vessels, the ability of West African trades to absorb this capacity will depend both on maintaining high growth rates for bauxite exports and the vessel age policy of charterers in the Simandou consortium once iron ore exports begin ramping up from 2025 onwards. Otherwise, older Capes may have to compete for limited cargoes, cannibalize the Kamsarmax trades, or finally be scrapped.

By Cara Hatton, Dry Bulk Analyst, Research.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business